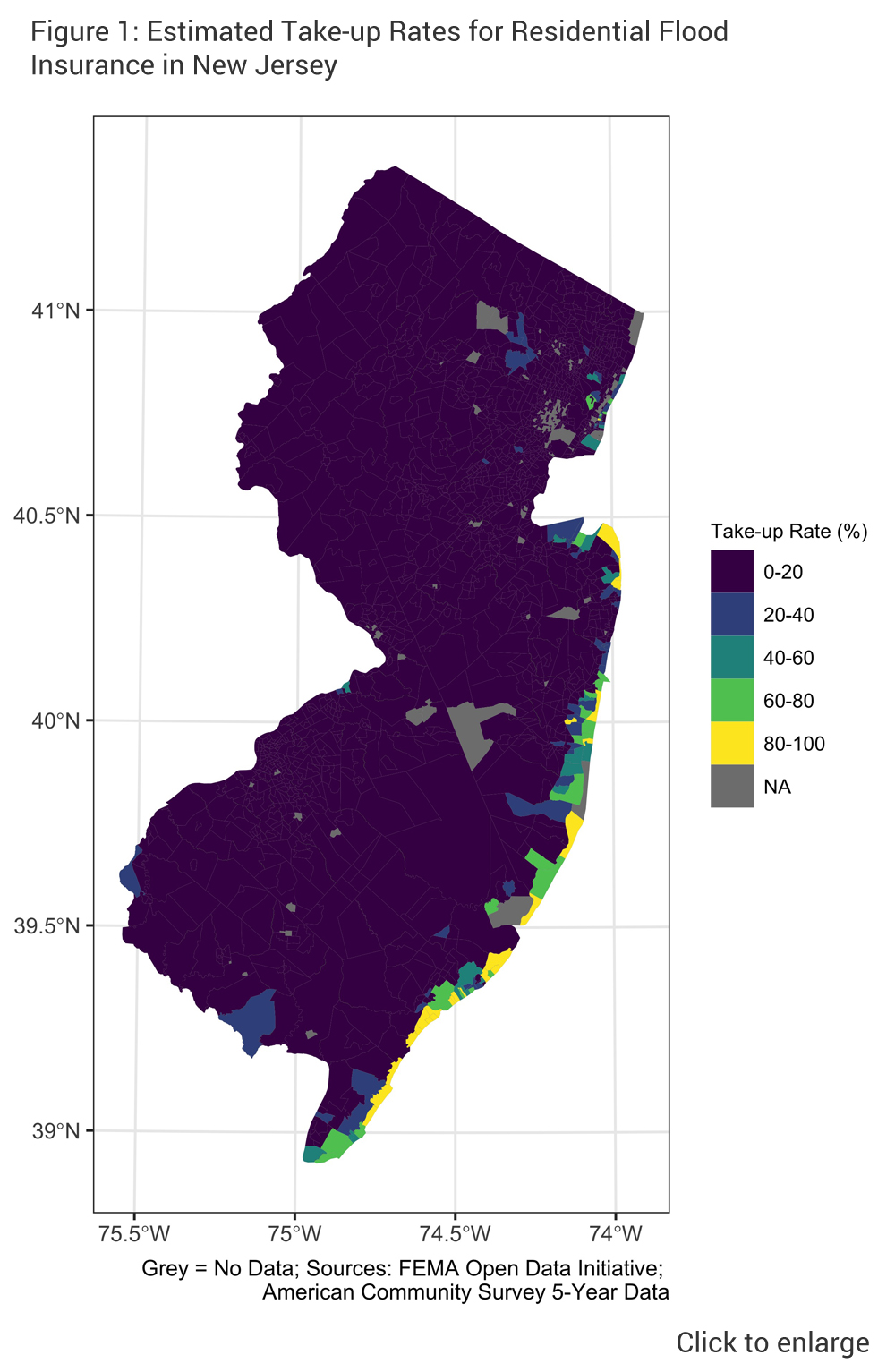

NFIP PURCHASES IN NEW JERSEY In New Jersey there were 250,561 policies-in-force (including both commercial and residential policies) across the state in 2018, the most recent full year for which data are available.7 This makes New Jersey fourth in the nation in terms of NFIP policies behind Florida, Texas, and Louisiana. NFIP policies tend to be concentrated in coastal areas. Figure 1 shows take-up rates for all NFIP policies in New Jersey by census tract (that is, the number of NFIP policies in each tract divided by the number of housing units in each tract). Note that census tracts are small areas of about 4,000 inhabitants and do not correspond to political boundaries. As seen in the figure, take-up rates are much lower away from the coast but can exceed 75% for tracts that border the ocean.

In New Jersey there were 250,561 policies-in-force (including both commercial and residential policies) across the state in 2018, the most recent full year for which data are available.7 This makes New Jersey fourth in the nation in terms of NFIP policies behind Florida, Texas, and Louisiana. NFIP policies tend to be concentrated in coastal areas. Figure 1 shows take-up rates for all NFIP policies in New Jersey by census tract (that is, the number of NFIP policies in each tract divided by the number of housing units in each tract). Note that census tracts are small areas of about 4,000 inhabitants and do not correspond to political boundaries. As seen in the figure, take-up rates are much lower away from the coast but can exceed 75% for tracts that border the ocean.

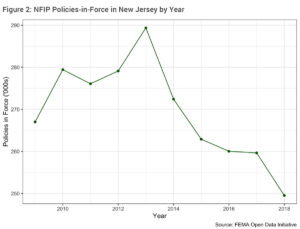

The number of policies-in-force in New Jersey has been declining in recent years as shown in Figure 2. Policies were increasing and then spiked after Hurricane Sandy; this could be due to greater purchases after the storm brought attention to flood risk, but also is due to the requirement that recipients of federal disaster aid purchase flood insurance.8 Due to a lack of comprehensive and detailed data on flood insurance provided by the private sector, it is impossible to determine how much of this recent decline has been offset by an increase in private-sector flood insurance policies.

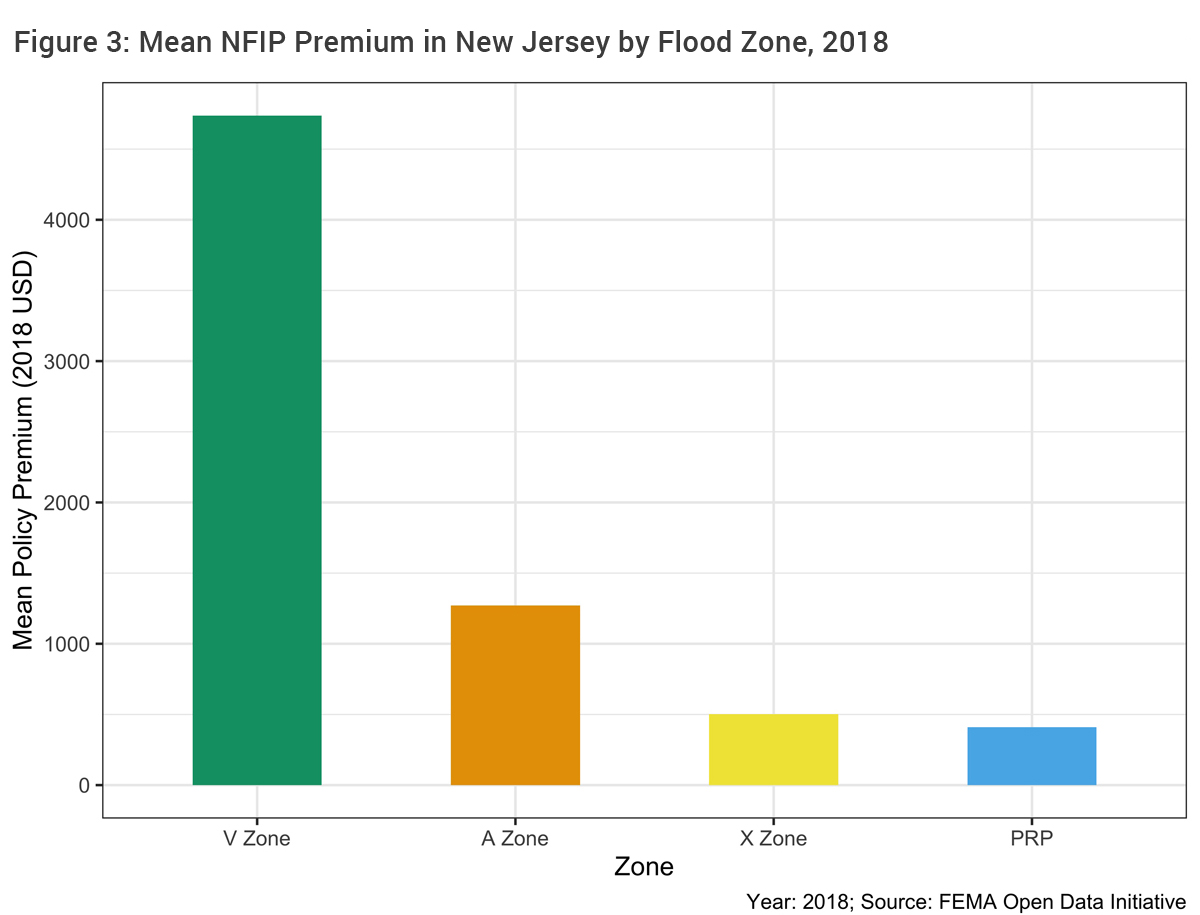

NFIP PREMIUMS

NFIP PREMIUMS

Currently, annual premiums for an NFIP policy vary by FEMA mapped flood zones, as well as by other characteristics of the building, including when it was constructed and its elevation. Figure 3 shows the average premiums for policies in New Jersey. The highest prices are for properties in the V zone – the area of the SFHA also subject to waves and storm surge. The average annual New Jersey premium in the V zone was $4,738 in 2018. In the A zone, the average premium was $1,272. Outside the SFHA, properties with a favorable loss history may qualify for a Preferred Risk Policy (PRP),9 which costs substantially less. The median for a PRP policy was $410. Note that premiums also vary based on how much coverage is purchased.

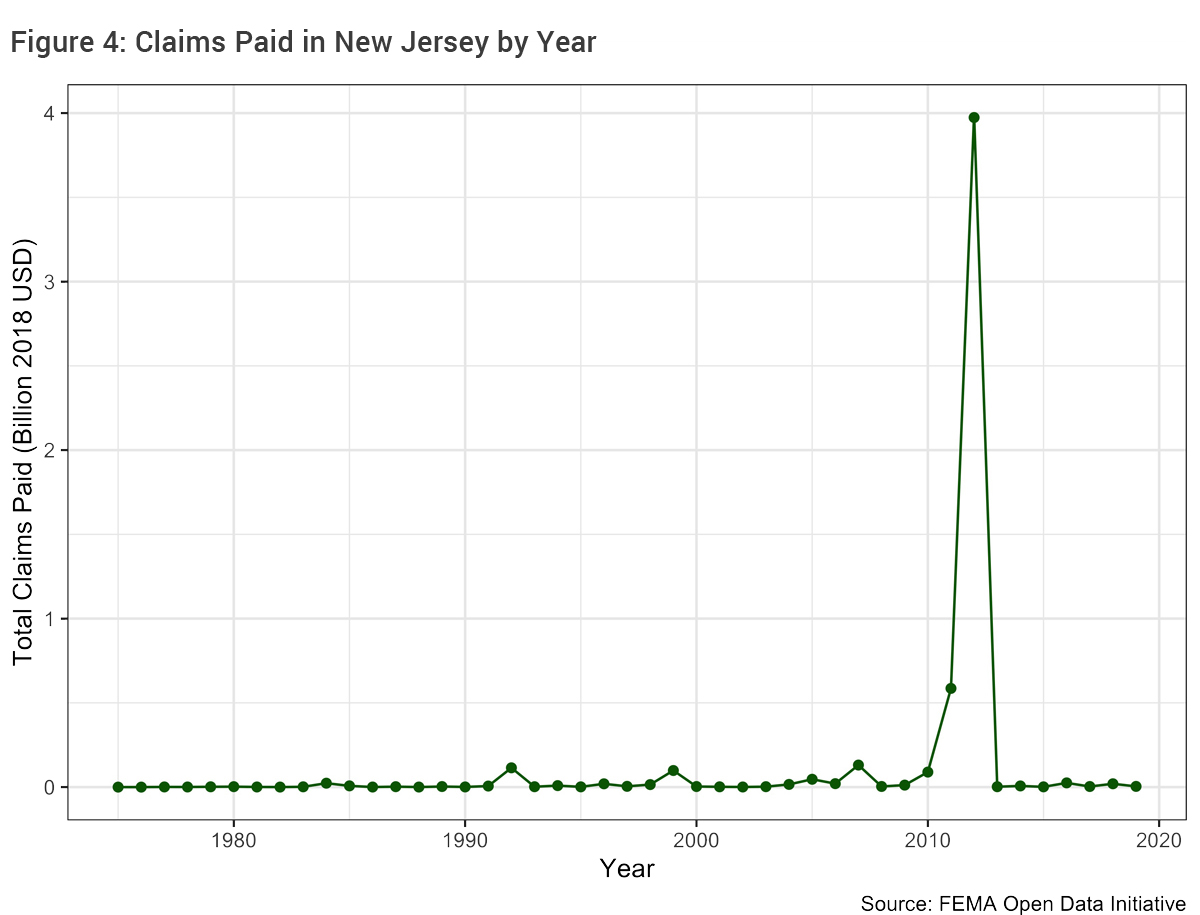

CLAIMS PAID

As of August 2019, New Jersey policyholders had cumulatively received roughly $5.268 billion (2018 USD) in total payments on 160,169 claims, only 7.57% of which were for commercial properties. The overwhelming majority of claims paid were in 2012 for Hurricane Sandy. This is seen clearly in Figure 4, which shows claims made to the state in billions of 2018 USD by year. The year Sandy hit – 2012 – shows close to $4 billion in losses paid on over 68,000 claims, only 3.94% of which were for commercial properties. (Larger firms may have comprehensive property insurance from a private carrier and not use the NFIP. Small businesses, though, are often uninsured and would use the NFIP for flood coverage similar to a household.)

As might be expected, given the storm, and the earlier figure showing where NFIP policies are concentrated, claims have largely been concentrated on the coast, as well. The most claims are in areas of higher take-up where Sandy had an impact – this is seen in Figure 5. In the week after Hurricane Sandy made landfall, the average claim was $151,244 (2018 USD) for commercial properties and $59,997 for residential properties. This highlights the importance of insurance in financial recovery from disasters. In contrast to the almost $60,000 that was paid on average for flood insurance claims, FEMA individual Assistance grants averaged only a bit more than $8,000 (which includes some funds for uninsured costs, such as temporary housing). This is because post-disaster FEMA grants are only to make homes safe and habitable, not bring them back to pre-disaster conditions.

As might be expected, given the storm, and the earlier figure showing where NFIP policies are concentrated, claims have largely been concentrated on the coast, as well. The most claims are in areas of higher take-up where Sandy had an impact – this is seen in Figure 5. In the week after Hurricane Sandy made landfall, the average claim was $151,244 (2018 USD) for commercial properties and $59,997 for residential properties. This highlights the importance of insurance in financial recovery from disasters. In contrast to the almost $60,000 that was paid on average for flood insurance claims, FEMA individual Assistance grants averaged only a bit more than $8,000 (which includes some funds for uninsured costs, such as temporary housing). This is because post-disaster FEMA grants are only to make homes safe and habitable, not bring them back to pre-disaster conditions.

THE COMMUNITY RATING SYSTEM

Since 1990, the NFIP has encouraged communities to join the Community Rating System (CRS), a voluntary program designed to encourage more investment in flood risk reduction. Class levels range from 1 to 10 with Class 1 providing the highest discount on premiums. A CRS community earns points for activities undertaken to better manage flood risk, including providing improved information on flood risk and flood insurance to residents. As a community moves up through levels in the program, their residents are rewarded with discounts on flood insurance. Note that PRP policies do not receive CRS discounts, as they are already a more favorable price. As of August 2019, 96 of the 553 New Jersey communities participating in the NFIP are in the CRS program. Many of these communities have a Class 5 or higher, indicating they have adopted many flood risk management policies. This includes Ocean City, Brigantine, Sea Isle City, and Long Beach.10

THE NFIP AND NEW JERSEY

As discussed, flood insurance is a critical component of financial recovery from flood events. Many households lack sufficient savings to rebuild on their own and federal aid is limited and delayed. Unfortunately, however, those who often need insurance the most are least able to afford it. FEMA and scholars have proposed a means-tested assistance program to help lower-income families afford flood coverage, but Congress has yet to adopt and enact this change.11 As climate change increases flood risk, particularly along the coast, flood insurance will also have to be complemented by aggressive investments in risk reduction and risk communication to promote resiliency of New Jersey communities.